Agentic Creation vs Agentic Buying: Two Futures of Commerce

Arron Young

Founder, Custyle · Apr 15, 2026·19 min read

Two Futures of Commerce

TL;DR: Everyone talks about AI agents that buy for you. Almost nobody talks about AI agents that create for you. These are two fundamentally different futures — with different economics, different trust dynamics, and different winners. The window for agentic creation is 2026-2028. After that, the giants arrive.

Table of Contents

- The Question Nobody Asks

- First Principles: Decision Cost

- Three Laws That Outlast Technology

- The Great Divergence

- C2A2M: Skip the Brand

- Six Layers, One Stack

- Category Sequencing Matters

- The Intent-to-Result Flywheel

- The 2026-2028 Window

- FAQ

The Question Nobody Asks

The entire agentic commerce conversation points in one direction. McKinsey projects $3-5 trillion in agentic commerce by 2030. OpenAI launched ACP. Google countered with UCP. Amazon built Rufus. ChatGPT now shops for 800 million weekly active users, driving over 20% of referral traffic to Walmart alone.

All of them solve the same problem: how to help AI find the best product from existing supply.

But here is the question nobody asks: what happens when the product you want does not exist yet?

"I want a birthday gift for a friend who loves space travel themes." No shelf holds the perfect answer. It needs to be created — not found.

That gap reveals two entirely different futures. Agentic creation vs agentic buying is not a branding exercise. It is a structural divergence with different economics, different moats, and different winners. This article maps the full framework — from first principles to competitive timing.

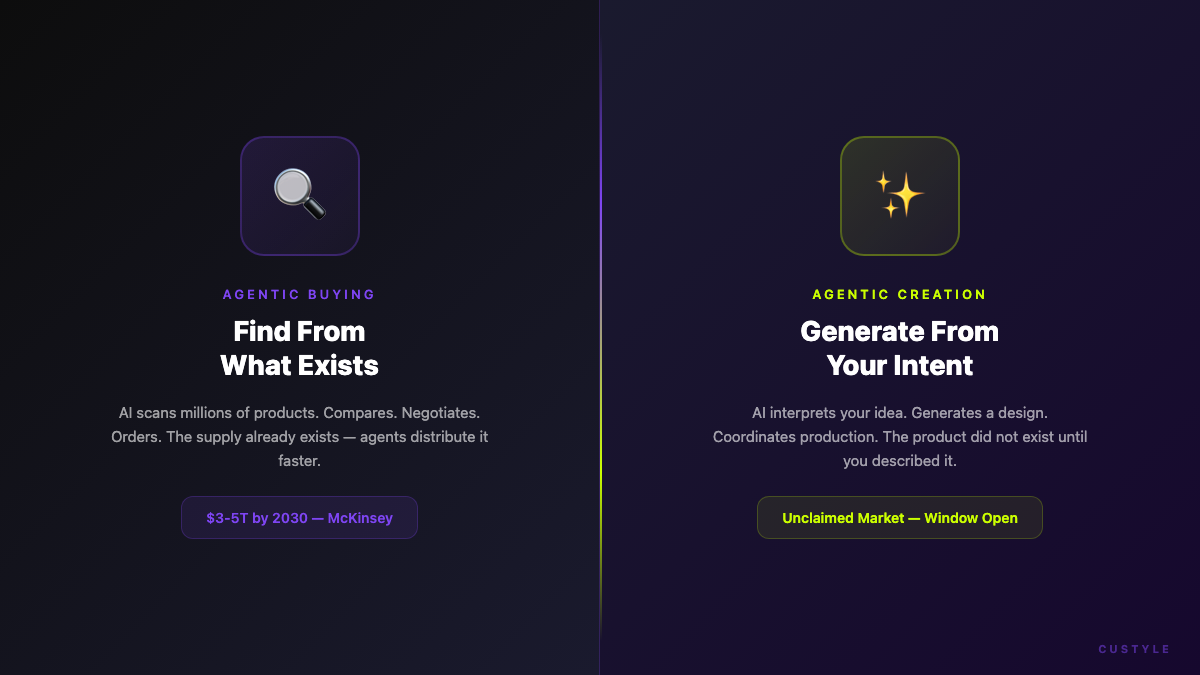

Two paths diverge: finding from existing supply vs generating new supply from intent.

Two paths diverge: finding from existing supply vs generating new supply from intent.

First Principles: Decision Cost

Most industry analysis defines retail as a "friction elimination system." That framing is useful but shallow. It describes symptoms, not the disease.

Retail's true first principle: compress the decision cost per unit of satisfaction. Friction is a symptom. Decision cost is the root.

This distinction matters because it explains two phenomena that "friction elimination" cannot:

Why does adding friction sometimes create value? Costco's membership, curated drops, limited releases — all increase friction. But they shrink the decision space. Fewer choices, higher trust, lower decision cost. "Friction elimination" calls these anomalies. Decision cost compression calls them strategy.

Why do custom products command a premium? Custom goods carry more friction — longer wait, higher price, more uncertainty. Yet they compress a deeper cost: the identity match. "Is this me?" When you participate in the design, the endowment effect resolves that question instantly.

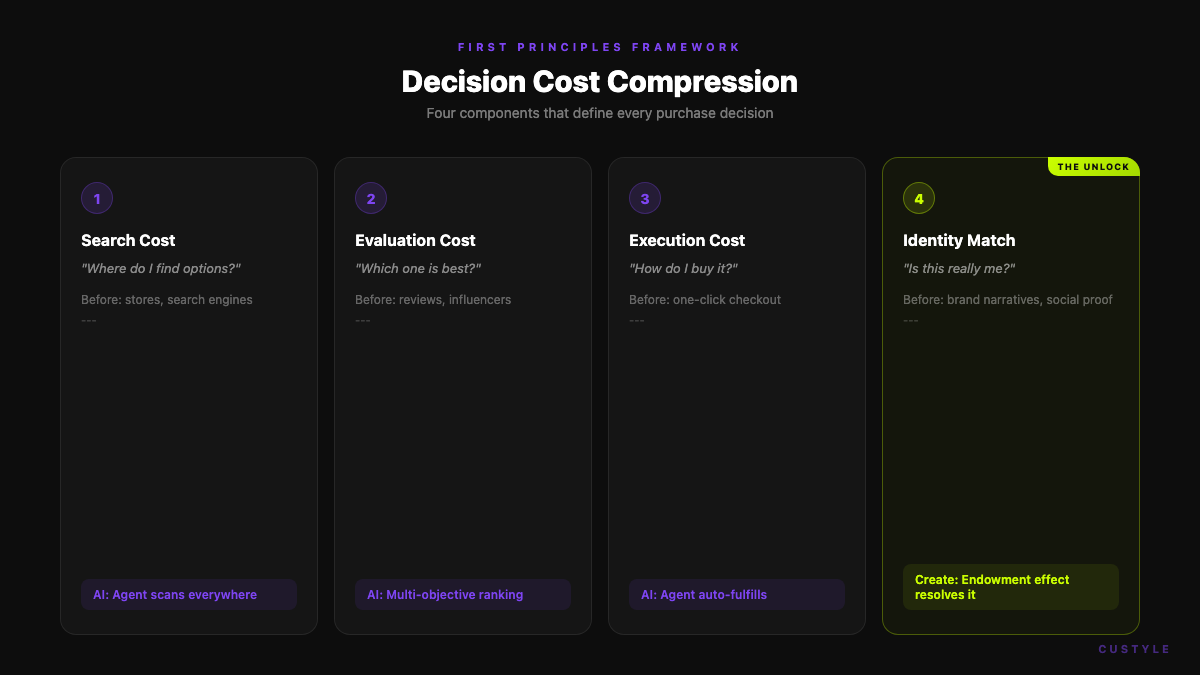

Four Components of Decision Cost

| Component | What It Means | Traditional Fix | AI-Native Fix |

|---|---|---|---|

| Search cost | Find candidates | Stores, search engines | Agent scans everywhere |

| Evaluation cost | Judge which is best | Reviews, influencers | AI multi-objective ranking |

| Execution cost | Complete the purchase | One-click checkout | Agent auto-fulfills |

| Identity match cost | "Is this me?" | Brand narratives, social proof | You participate in creation — endowment effect resolves it |

The fourth component is the key. The emotion economy reaches $2.3 trillion. 55% of consumers buy based on recommendations. Gen-Z pays premiums for identity-matched products. All these data points share one root: people pay to reduce the uncertainty of "is this me?"

Custom products compress identity match cost to near zero. That is not a guess — it is a structural advantage derived from behavioral economics.

Four components of decision cost — and why identity match is the unlock for agentic creation.

Four components of decision cost — and why identity match is the unlock for agentic creation.

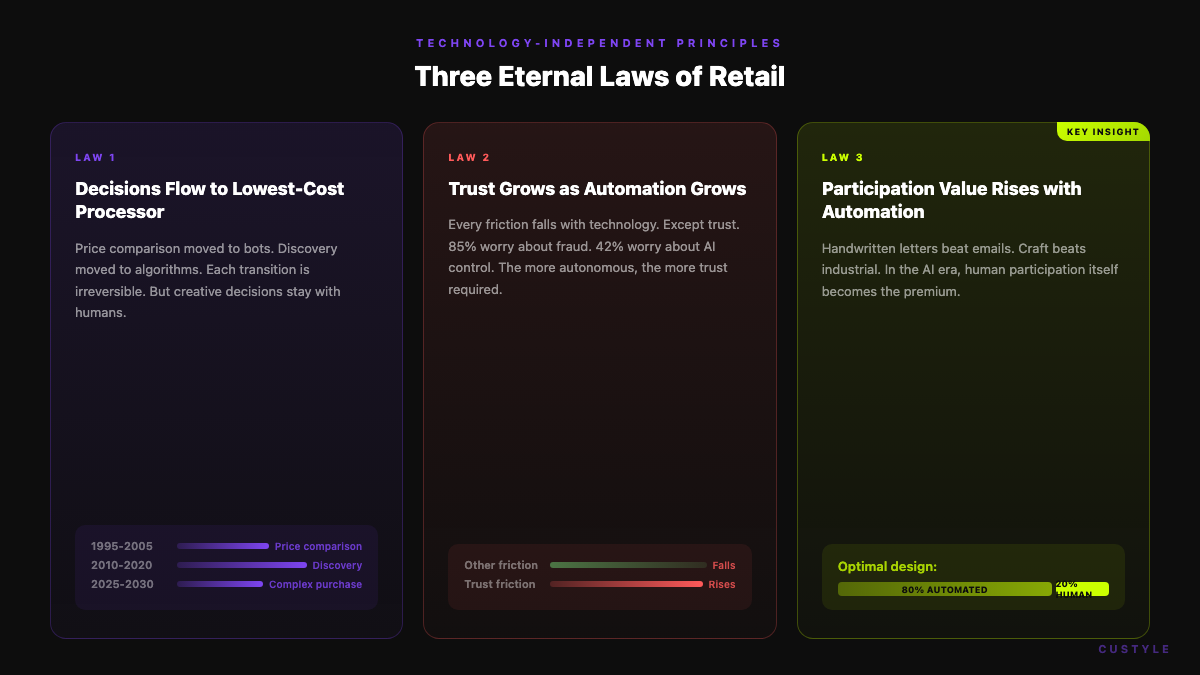

Three Laws That Outlast Technology

Cross-referencing ten global research reports reveals three laws that hold across every retail paradigm shift. They do not depend on any specific technology. They will hold for 20+ years.

Law 1: Decisions Flow to the Lowest-Cost Processor

Price comparison moved from store visits to comparison websites (1995-2005). Product discovery moved from ads to recommendation algorithms (2010-2020). Daily restocking moves to AI auto-replenishment (2025-2030). Complex purchases move to AI multi-objective reasoning (2026-2032).

Each transition is irreversible. Once a lower-cost processor exists, decisions never flow back.

But notice the exception: creative design decisions will not fully transfer to machines. Humans and AI will co-create. This exception defines the entire agentic creation space.

Law 2: Trust Is the Only Friction That Grows with Automation

Every other friction falls as technology improves. Trust moves in the opposite direction. 85% of Americans worry about online fraud. 42% worry about AI losing control. The more autonomous the agent, the more trust you need.

Trust is not a product feature. It is infrastructure. The "agent trust stack" includes four layers: auditable, revocable, compensable, and accountable. Whoever productizes trust first builds the next generation of commerce infrastructure.

Law 3: Participation Value Rises with Automation

This is the most counterintuitive law. As AI handles more routine decisions, the decisions humans choose to participate in become more valuable. A handwritten letter carries more weight than an email. A craft beer costs more than an industrial one.

In the AI era, human participation itself becomes the premium.

The design implication: the best product is not 100% automated. It is 80% automation plus 20% meaningful human participation. Too many custom platforms die because the creation bar is too high. But full automation also fails — it strips the dopamine, the endowment effect, the joy of "I made this."

This is what we call beneficial imperfection: deliberately designed participation at the right moments.

Three laws that hold across every paradigm shift — and why the third one matters most for creators.

Three laws that hold across every paradigm shift — and why the third one matters most for creators.

The Great Divergence

Here is the core thesis: commerce has two endgames, not one. Nearly every dollar of investment in agentic commerce flows into one side. The other side remains unclaimed.

Agentic Buying: Find the Best From What Exists

AI scans millions of existing products, compares prices, reads reviews, negotiates, and places orders. The supply already exists. The agent distributes it more efficiently.

Players: ChatGPT Shopping, Amazon Rufus, Google Gemini, Perplexity Shopping. Market size: $3-5 trillion by 2030, per McKinsey.

Agentic Creation: Generate What Does Not Exist Yet

AI interprets your intent, generates a design, maps it to production parameters, coordinates manufacturing, and delivers a product that did not exist before you expressed the idea. The supply is born from intent.

Players: no clear leader. Market size: not yet estimated — but print-on-demand alone is a $45 billion single-category market growing at 11% CAGR.

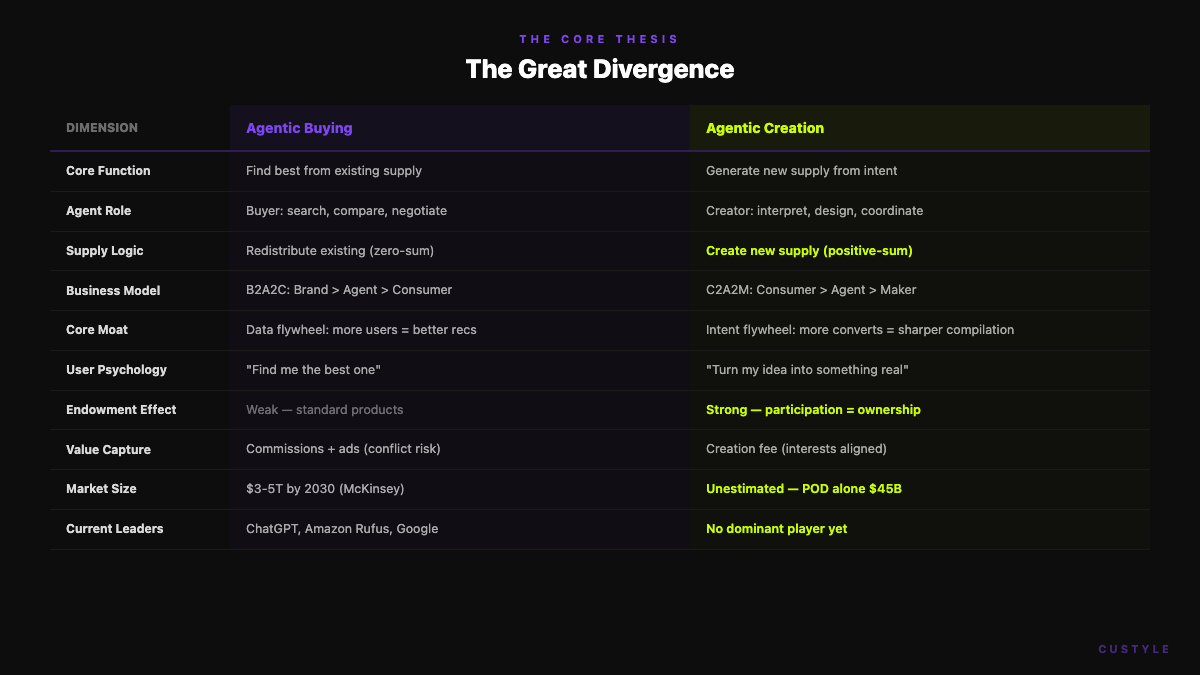

Side-by-Side Comparison

| Dimension | Agentic Buying | Agentic Creation |

|---|---|---|

| Core function | Find the best from existing supply | Generate new supply from intent |

| Agent role | Buyer: search, compare, negotiate, order | Creator: interpret intent, generate design, match process, coordinate production |

| Supply logic | Distribute existing supply (zero-sum) | Create new supply (positive-sum) |

| Business model | B2A2C: Brand to Agent to Consumer | C2A2M: Consumer to Agent to Manufacturer |

| Moat | Data flywheel: more users, better recommendations | Intent flywheel: more conversions, sharper intent compilation, irreplicable domain knowledge |

| User psychology | "Find me the best one" — cognitive offloading | "Turn my idea into something real" — creative participation |

| Endowment effect | Weak: standard products, no emotional bond | Strong: design participation triggers ownership feeling, lower returns |

| Value capture | Commission and ads (conflict-of-interest risk) | Creation service fee (aligned: your satisfaction equals our revenue) |

| Market size | $3-5T by 2030 (McKinsey) | Unestimated. POD single category: $45B, 11% CAGR |

| Current leaders | ChatGPT Shopping, Amazon Rufus, Google Gemini | No dominant player — the window is open |

The billions invested globally in agentic commerce all sit on the buying side. The creation side has no leader. Not because the opportunity is small — but because it requires a rare intersection: AI intent compilation and flexible manufacturing coordination. Very few stand at that crossroads.

Every major player bets on agentic buying. Agentic creation remains an open field.

Every major player bets on agentic buying. Agentic creation remains an open field.

C2A2M: Skip the Brand

Traditional e-commerce: B2C. Brand builds, consumer buys.

Agentic buying reshuffles the chain: B2A2C. Brand builds, agent finds, consumer receives.

Agentic creation does something more radical. It introduces C2A2M: Consumer to Agent to Manufacturer. The consumer expresses intent. The agent compiles it into production parameters. The manufacturer builds it. The brand layer disappears entirely.

This restructuring changes the economics fundamentally:

- Traditional retail is zero-sum. Brand A's gain is Brand B's loss. Same products, different shelves.

- C2A2M is positive-sum. Every custom product adds new supply to the world. It does not steal share from existing brands. It creates share that did not exist.

The implications for the future of commerce 2026 and beyond are massive. In a C2A2M world, the valuable entity is not the brand. It is the agent that compiles intent into reality. The agent owns the relationship, the data, and the flywheel.

-> Related: What Is an AI Merch Agent?

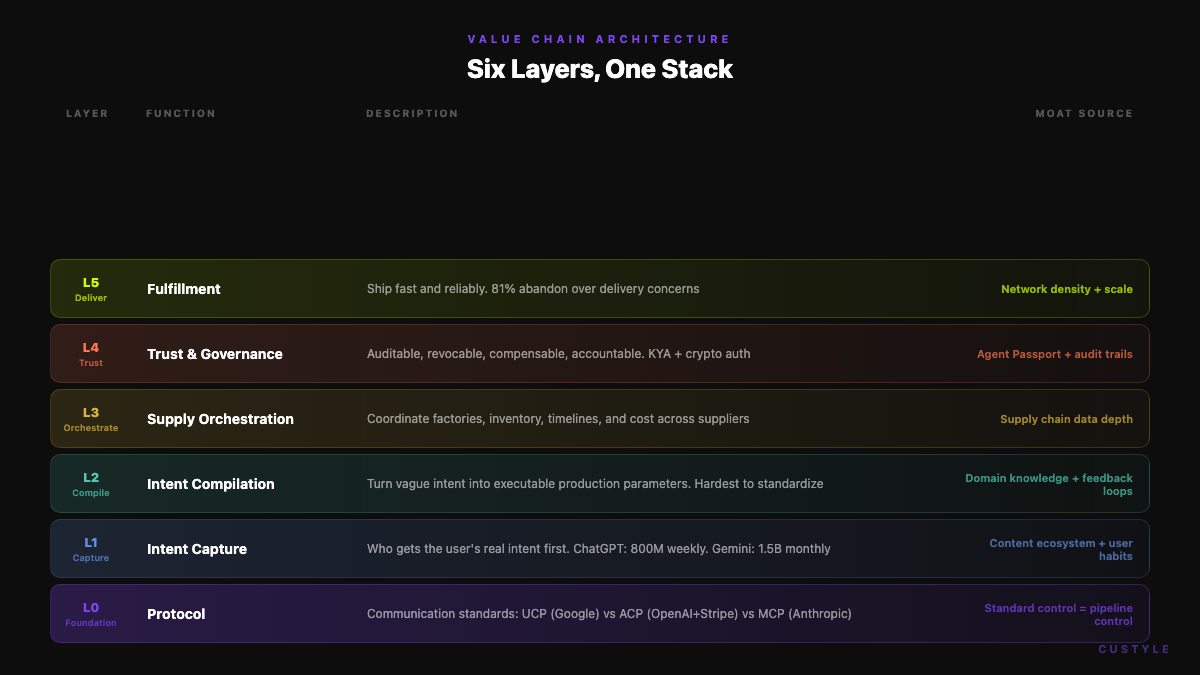

Six Layers, One Stack

The retail value chain is being re-layered. Each layer has its own moat. Pay special attention to L0 — protocols are the new battleground.

| Layer | Function | Moat Source | Current State |

|---|---|---|---|

| L0: Protocol | Communication standards between agents and merchants | Standard control = pipeline control. UCP (Google) vs ACP (OpenAI + Stripe) vs MCP (Anthropic) | Protocol wars have started. Comparable to early HTTP vs alternatives |

| L1: Intent Capture | Who gets the user's real intent first | Content ecosystems, user habits, traffic entry points | ChatGPT: 800M weekly actives. Gemini: 1.5B monthly reach |

| L2: Intent Compilation | Turn vague intent into executable parameters | Domain knowledge graphs, production constraint mapping, intent-to-result feedback loops | Hardest to standardize. Highest moat value |

| L3: Supply Orchestration | Coordinate factories, inventory, timelines, cost | Supply chain data depth, multi-supplier coordination | Multi-objective balancing: flexibility vs cost vs speed |

| L4: Trust & Governance | Auditable, revocable, compensable, accountable | KYA (Know Your Agent), cryptographic authorization, audit trails | Agent Passport, Visa Agentic Ready |

| L5: Fulfillment | Ship it fast and reliably | Network density, automation, scale economics | 81% of consumers abandon purchases over delivery concerns |

Protocol wars are replacing page wars. Whether your product catalog is ACP/MCP-compatible will determine whether AI agents can even discover you. This is the infrastructure battle of the decade.

The L1-L2 feedback loop deserves attention. Without intent capture, the compiler has no feed. Without compilation, intent has no monetization path. Companies that can only build but cannot capture demand sink into infrastructure. Companies that capture demand but cannot deliver sink into hollow traffic.

The future of commerce 2026 belongs to whoever closes both loops.

From Protocol (L0) to Fulfillment (L5) — the new value chain of agentic commerce.

From Protocol (L0) to Fulfillment (L5) — the new value chain of agentic commerce.

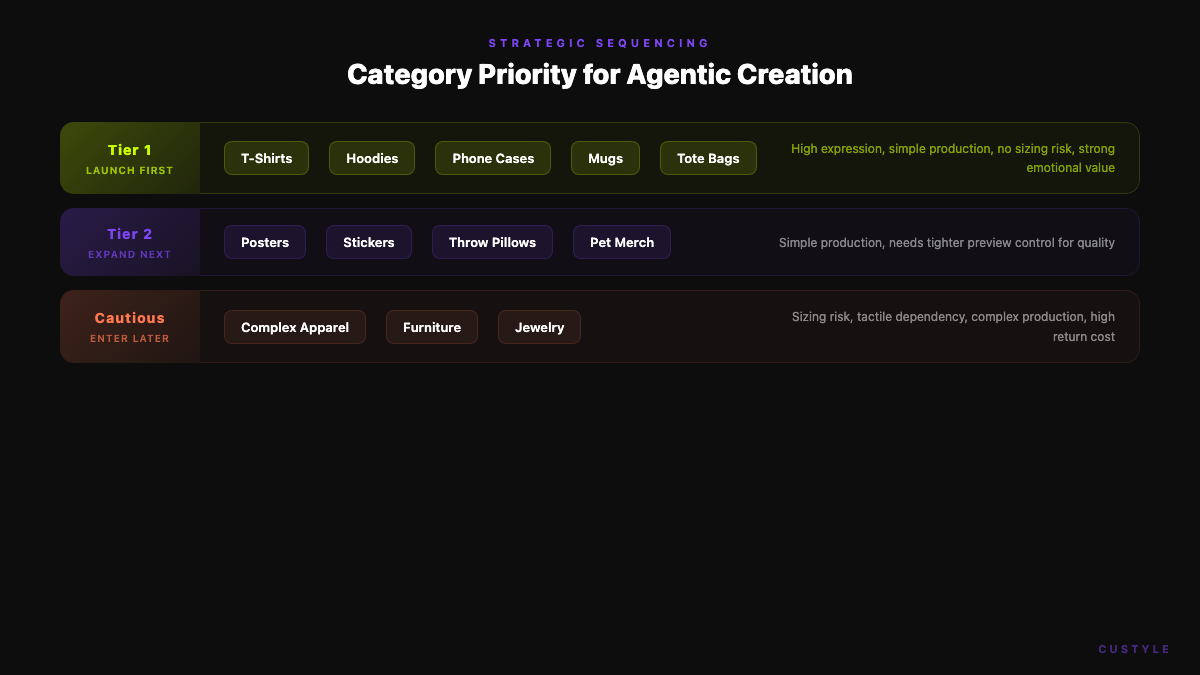

Category Sequencing Matters

Agentic creation is not an abstract thesis. It is a category war where sequence determines survival. The first categories to fall share three traits: high design variability, low production complexity, and strong emotional value.

| Priority | Categories | Use Cases | Why First |

|---|---|---|---|

| Tier 1 | T-shirts, hoodies, phone cases, mugs, tote bags | Fandom merch, gifts, team culture, self-expression | High design freedom. Simple production. No sizing risk. Strong emotional value |

| Tier 2 | Posters, stickers, throw pillows, pet merch | Promotional materials, home decor, pet expression | Simple production, but needs tighter preview control |

| Cautious | Complex apparel, furniture, jewelry | High-ticket but high-risk | Sizing risk, tactile dependency, complex production, high return cost |

AI plus C2M will not eat "all of retail" first. It will eat the categories where expression is high, manufacturing is simple, and previews are controllable. Build a repeatable intent-to-delivery loop there — then expand.

This is why merch is the proving ground. T-shirts, hoodies, phone cases — these are high-expression, low-complexity products. They let you build the flywheel without the risk of complex manufacturing. Custyle.ai, as the AI Merch Agent, starts here deliberately. Not because the ambition is small — because the sequencing is strategic.

Tier 1 categories combine high expression with low production complexity — the ideal starting point.

Tier 1 categories combine high expression with low production complexity — the ideal starting point.

The Intent-to-Result Flywheel

Traditional retail runs on the SKU flywheel: more SKUs attract more users, more users generate more data, better data drives better recommendations. In agentic creation, the core asset is not SKU count. It is the precision of intent-to-result mapping.

The most valuable data in this new model is not "how many units of this SKU sold." It is:

- What kind of vague expression maps to which design style?

- Which user segments convert on which proposals?

- Which previews produce lower return rates?

- Which delivery promises drive repeat purchases?

Once this flywheel starts spinning, it becomes a "vibe to merch" operating system. The real network effect is not "more users make it cheaper." It is "more users make the compilation sharper, and sharper compilation makes the experience better."

Three KPIs That Determine Survival

| KPI | Definition | Why It Is Critical |

|---|---|---|

| Preview Accuracy | Match between preview image and physical product | Directly determines return rate. A 10% improvement can reduce returns by 30%+ |

| Intent-to-Fulfillment Time | Total time from expressing intent to receiving the product | Currently 7-21 days. Compressing to 3-5 days would be a major breakthrough |

| 30-Day Repeat Rate | Percentage of buyers who return within 30 days | Above 15% validates the model. Above 25% means the flywheel is turning |

95.5% of enterprises have deployed at least one AI commerce capability. But most remain at Level 2 — basic intent understanding with human-assisted execution. The leap to Level 3, where agents plan, execute, and reflect in closed loops, defines the next competitive frontier.

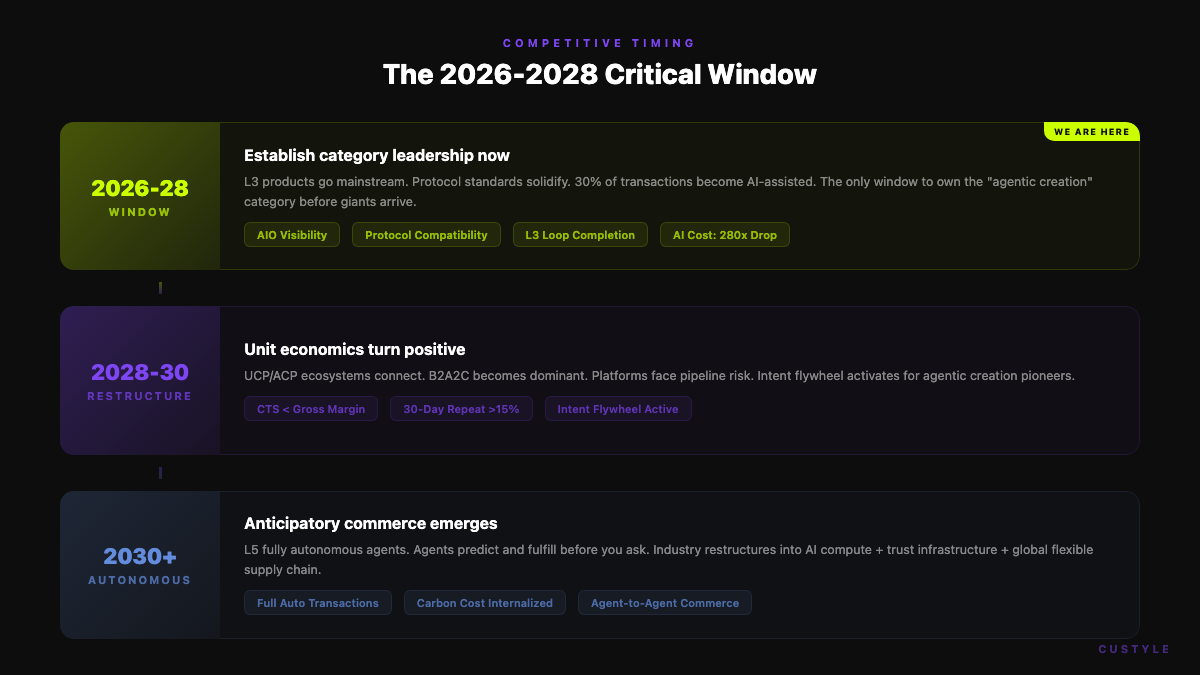

The 2026-2028 Window

McKinsey's warning bears repeating: "When changes in customer behavior become visible in e-commerce KPIs, laggards may already be too late to catch up."

Four curves converge between 2025 and 2028:

- Intelligence cost collapse. AI inference costs dropped 280x in 18 months. The computational barrier to agentic creation is dissolving.

- Supply chain flexibility. China accounts for 54% of global industrial robot installations. Flexible manufacturing infrastructure is mature.

- Consumer demand certainty. The emotion economy is $2.3 trillion. Identity-matched products are not a niche — they are a confirmed market.

- Protocol infrastructure. ACP, UCP, MCP, AP2 — the communication standards for agents are forming now.

Timeline

| Phase | Period | What Happens | Key Metrics |

|---|---|---|---|

| Window | 2026-2028 | L3 products go mainstream. Protocol standards solidify. 30% of transactions are AI-assisted. For agentic creation: the only window to establish category leadership | AIO visibility, protocol compatibility, L3 loop completion |

| Restructuring | 2028-2030 | UCP/ACP ecosystems connect. B2A2C becomes the dominant model. Platforms face "pipeline risk." For agentic creation: unit economics turn positive, intent flywheel activates | Cost-to-serve below gross margin. 30-day repeat rate above 15% |

| Autonomous | 2030+ | L5 fully autonomous agents. "Anticipatory commerce" — agents predict and fulfill before you ask. Industry restructures into three stable layers: AI compute, trust infrastructure, global flexible supply chain | Fully automated transaction share. Carbon cost internalization |

ChatGPT already reaches 800 million weekly active users and sends 20%+ traffic to Walmart. When these general-purpose agents start handling custom products, the window closes. First-mover advantage lies in three assets built over time: deeper intent understanding, accumulated user trust, and mature AI-to-production parameter mapping.

Three phases: Window (2026-2028), Restructuring (2028-2030), Autonomous (2030+).

Three phases: Window (2026-2028), Restructuring (2028-2030), Autonomous (2030+).

Where Custyle Stands

On the agentic buying side, the giants have arrived. ChatGPT, Amazon, Google — billions of dollars deployed.

On the agentic creation side, the field is open. Custyle.ai is building here — at the intersection of AI intent compilation and flexible manufacturing coordination. The AI Merch Agent turns vague expressions into real products: you describe a vibe, and the system handles creative direction, design, production process selection, and delivery.

The strategy follows the framework in this article precisely:

- Category sequencing: Start with Tier 1 merch — t-shirts, hoodies, phone cases. High expression, low complexity.

- Beneficial imperfection: 80% automation, 20% meaningful participation. You choose, you adjust, you feel ownership. Thirty seconds to "this is mine" — not thirty minutes playing designer.

- Intent flywheel: Every conversion sharpens the compilation. Every return teaches the preview system. The data asset is not SKU count — it is intent-to-result mapping precision.

- C2A2M economics: Positive-sum. Every product is new supply, not redistribution.

The five-sentence summary of this entire research:

- Retail's essence is decision cost compression. Not friction elimination.

- Commerce has two endgames. Agentic buying distributes existing supply. Agentic creation generates supply that never existed. The first is $3-5 trillion. The second has not been estimated.

- Protocol wars replace page wars. Whether your products are agent-readable determines whether you are discoverable.

- Category sequencing determines survival. Start where expression is high, manufacturing is simple, and previews are controllable.

- The endgame is not "more products." It is less thinking, higher certainty, and more "like me."

Missing this window does not mean earning less profit. It means being excluded from the next paradigm entirely.

-> Related: From Taste to Tangible — How Custyle Works -> Related: The Creator Economy Needs AI Merch

FAQ

What is agentic creation vs agentic buying?

Agentic buying means AI agents find and purchase the best product from existing inventory on your behalf. Agentic creation means AI agents generate entirely new products from your intent — designing, matching production processes, and coordinating manufacturing for items that did not exist before you described them. The first redistributes supply. The second creates it.

How big is the agentic commerce market?

McKinsey projects agentic commerce will reach $3-5 trillion by 2030. That estimate covers agentic buying — agents finding products from existing supply. Agentic creation has not been separately estimated, but print-on-demand alone represents a $45 billion market growing at 11% CAGR, validating core demand.

What is the C2A2M model?

C2A2M stands for Consumer to Agent to Manufacturer. Unlike B2C (brand sells to consumer) or B2A2C (brand sells through agent to consumer), C2A2M skips the brand layer entirely. You express intent, the AI agent compiles it into production parameters, and the manufacturer builds it. Every product is new supply — making it a positive-sum model rather than a zero-sum redistribution.

Why does category sequencing matter for AI commerce?

Not all product categories are equally ready for agentic creation. Categories with high design freedom, simple manufacturing, and low return risk should come first. T-shirts, hoodies, and phone cases fit perfectly — they allow high expression, require no complex sizing, and carry strong emotional value. Starting here builds the intent-to-result flywheel before expanding to harder categories.

Why is 2026-2028 the critical window?

Four curves converge: AI inference costs dropped 280x in 18 months, flexible manufacturing infrastructure matured (China holds 54% of global industrial robot installations), consumer demand for identity-matched products is confirmed ($2.3T emotion economy), and agent communication protocols (ACP, UCP, MCP) are forming now. Once general-purpose agents like ChatGPT begin handling custom products, the window for specialist builders closes.

Ready to make something?

Turn your ideas into real merch with AI. No design skills needed.

Start with a vibeArron Young

Founder, Custyle · Apr 15, 2026·19 min read

Further Reading

Explore all →

Turn Your Pet's Photo Into Wearable Merch in Minutes (AI-Powered)

Turn one photo of your pet into a styled portrait and real wearable merch in minutes. Photo tips, style picks, print specs, and the AI shortcut that does it all in one chat.

Read more →Put a Legend's Name on Your World Cup Jersey

The official store said no. Messi, a retired legend, grandpa's name — here's the tribute World Cup jersey the store won't make you. Any name, any number.

Read more →

How to Make a Custom World Cup Jersey With AI (2026)

A custom World Cup jersey with AI means any name, any number, real typography — printed onto a real jersey and shipped, not a mockup. Here's how to make yours for 2026.

Read more →The Future of Brand Identity in AI Commerce: When Every Buyer Has an Agent

AI agents were supposed to demote brands to a backend API. The 2026 data says the opposite: AI sends high-intent buyers straight to brand.com. The new question is what you make.

Read more →