The Endgame of Commerce: Agentic Creation Is the Trillion-Dollar Frontier

Arron Young

Founder, Custyle · May 19, 2026·19 min read

The Endgame of Commerce: Agentic Creation Is the Trillion-Dollar Frontier

TL;DR Every top AI lab is building Agentic Buying — AI that finds you the best product. The bigger blue ocean is Agentic Creation — AI that generates a product that did not exist before. Two parallel paradigms, completely different economics. The window to lead the creation side is 2026–2028.

By Arron Young — Founder, Custyle. Previously AI Strategy at JD.com.

Key Takeaways

- The channel-migration era is over. China's online retail penetration sits at 26.1%. With 974M online shoppers and 1.04B short-video users, the offline-to-online runway is gone. Growth now comes from the supply system, not the channel.

- The global consensus is solving the wrong problem. McKinsey's $3–5T forecast, OpenAI's ACP, Google's UCP, Amazon Rufus — all of it is Agentic Buying. Nobody serious is building Agentic Creation.

- C2A2M skips the brand layer. Traditional commerce is B2C. Agentic Buying is B2A2C. Agentic Creation is C2A2M — Consumer → Agent → Manufacturer, with brands cut out entirely.

- Protocol wars are replacing page wars. ACP, UCP, MCP, AP2, A2A — the new HTTP fight. If your catalog isn't Agent-readable, AI won't find you.

- The window is 2026–2028. Four curves converge: inference cost down 280x, China's 2.027M-robot flexible manufacturing, the $2.3T emotion economy, and protocol-layer standardization. After that, ChatGPT's 800M weekly active users absorb the category.

Why This Report Is Different

For ten years, retail's central story was channel migration — offline to online, PC to mobile, search to content. That story is finished.

China's physical-goods e-commerce now represents 26.1% of total retail sales (National Bureau of Statistics, 2025). The ceiling is here. Growth no longer comes from moving stores online. It comes from rebuilding the supply system underneath.

Right now, every serious player in AI commerce is solving the same question: How do we make AI find the right product faster? McKinsey's celebrated $3–5T forecast, OpenAI's Agentic Commerce Protocol, Google's Universal Checkout Protocol, Amazon Rufus, ChatGPT Shopping — all of them optimize the search → compare → buy loop. They make existing supply more efficient.

But there's a second paradigm hiding in plain sight: AI doesn't search for the product. AI generates one that didn't exist.

This is not buying-automation. It is creation-automation. The economics, trust dynamics, and moats are completely different.

This is the gap Custyle was built to own. The rest of this report explains why the creation side is the real frontier — and why the window is closing fast.

1. The Channel Migration Story Is Dead

The three biggest markets all hit penetration ceilings at the same time:

| Market | E-commerce Penetration | Source |

|---|---|---|

| China | 26.1% of retail sales | NBS 2025 |

| United States | 16.4% of retail sales | U.S. Census 2025 |

| Europe (EU) | 78% of internet users buy online | Eurostat 2024 |

When the user-growth fuel runs out, the competitive logic flips. Winners are no longer the teams that "ran traffic best." They're the teams that rewrote the supply system.

That shift moves the scorecard from front-end metrics to four new ones:

- Forecast precision — JD's supply-chain LLM hit 92% demand-forecast accuracy in 2025.

- Flexible supply response — SHEIN ships from concept to shelf in 7–14 days.

- Fulfillment certainty — 30-minute delivery is becoming a baseline expectation.

- Reverse logistics efficiency — return cost is now the largest controllable variable in cost-to-serve.

Supply-chain capability is replacing traffic operations as the core valuation driver in retail.

2. Retail's First Principle: Compress Decision Cost

Most analysts describe retail as a friction-elimination system. That's correct but shallow. The deeper truth: retail's first principle is decision-cost compression — lowering the cost per unit of satisfaction.

Friction is the symptom. Decision cost is the disease. This matters because "friction elimination" can't explain two stubborn counterexamples — and a theory that can't explain edge cases isn't ready.

Counterexample one — Costco. Costco charges a membership fee just to walk in (more friction). Yet it has 130M+ paying members with >90% renewal. Curated assortment removes 90% of SKUs (more search friction). The result: faster decisions and higher repeat rates.

Counterexample two — custom products. Custom items take longer, cost more, and carry higher uncertainty. By any "friction elimination" model, they should lose. They don't. Because they compress a deeper cost: identity-match cost — the cost of confirming "this is me."

The Four Components of Decision Cost

| Component | What it means | AI-native answer | Custom-product answer |

|---|---|---|---|

| Search | Finding candidates | Agent crawls the web | No search — the product doesn't exist yet |

| Evaluation | Judging which is good | Agent multi-objective optimization | Agent generates options and explains tradeoffs |

| Execution | Closing the transaction | Agent auto-checkout, protocol-level | Production lead time is the real bottleneck |

| Identity match | Confirming "this is me" | Personalized recommendations | Endowment effect drops it close to zero |

Identity-match cost is the hidden engine behind the $2.3T emotion economy, the 55% of consumers who buy from recommendations, and Gen Z paying more for goods that match their taste. Custom products compress it through the endowment effect — and that is the economic floor under Agentic Creation.

3. Three Eternal Laws of Retail

Ten independent research reports cross-validate three rules. They don't depend on any specific technology, so they hold for 20+ years.

First Law — Decision cost flows to the lowest-cost processor

Whenever a new "decision processor" — human brain, store clerk, search engine, recommendation algo, AI agent — can handle a decision more cheaply, the decision migrates to it.

| Decision | Old processor | New processor | Window | Reversible? |

|---|---|---|---|---|

| Price comparison | Human walking stores | Search engines | 1995–2005 | No |

| Product discovery | Ads + clerks | Recommendation algorithms | 2010–2020 | No |

| Routine restocking | Memory + manual order | AI agent auto-restock | 2025–2030 | In progress |

| Complex purchase | Human research | AI agent multi-objective | 2026–2032 | Early |

| Creative judgment | Human taste | AI + human co-creation | 2025–2035 | Never fully transfers |

That last row is the doorway to Law 3. Creative judgment is the only category where automation does not fully replace humans.

Second Law — Trust is the only friction that grows with automation

Every other friction goes down as technology improves. Trust runs the opposite direction.

- 85% of U.S. adults consider online scams a problem (Pew 2025).

- 42% of consumers worry about AI shopping going off the rails (Checkout.com).

- 47% trust AI for essentials — but only in low-risk standard goods (Walmart research).

- AI-payment psychological authorization caps: £204 UK / $233 US (Checkout.com).

These numbers aren't contradictory — they're layered. Consumers will trust AI for replenishment commodities. They will not trust AI for high-stakes purchases without a kill switch.

Trust is not a feature. Trust is infrastructure. The "Agent Trust Stack" needs four minimums: auditable, revocable, refundable, attributable. Whoever productizes that stack first becomes the utility layer of next-gen commerce.

Visa Agentic Ready, Mastercard Agent Pay, and Stripe ACP aren't payment features. They're the trust stack going live. That's the most under-priced infrastructure bet of 2026.

Third Law — Participation grows in value as automation rises

This is the counterintuitive one. The empirical backing is strong:

- Endowment Effect (Kahneman, Knetsch & Thaler, 1990) — people value owned items roughly 2x unowned identical items.

- IKEA Effect (Norton, Mochon & Ariely, 2012) — people will pay 63% more for objects they helped assemble, imperfections and all.

- Flow (Csikszentmihalyi) — activities slightly above skill level produce the highest subjective value.

When AI handles the boring 80%, the 20% you choose to do yourself becomes scarce — and therefore valuable.

Design rule that falls out of this: The best products are 80% automated + 20% meaningful human participation. Full automation strips away the endowment effect. Full DIY scares 95% of users out of the funnel. Most custom platforms die from setting the creation bar too high. The fix isn't more automation — it's better-shaped participation.

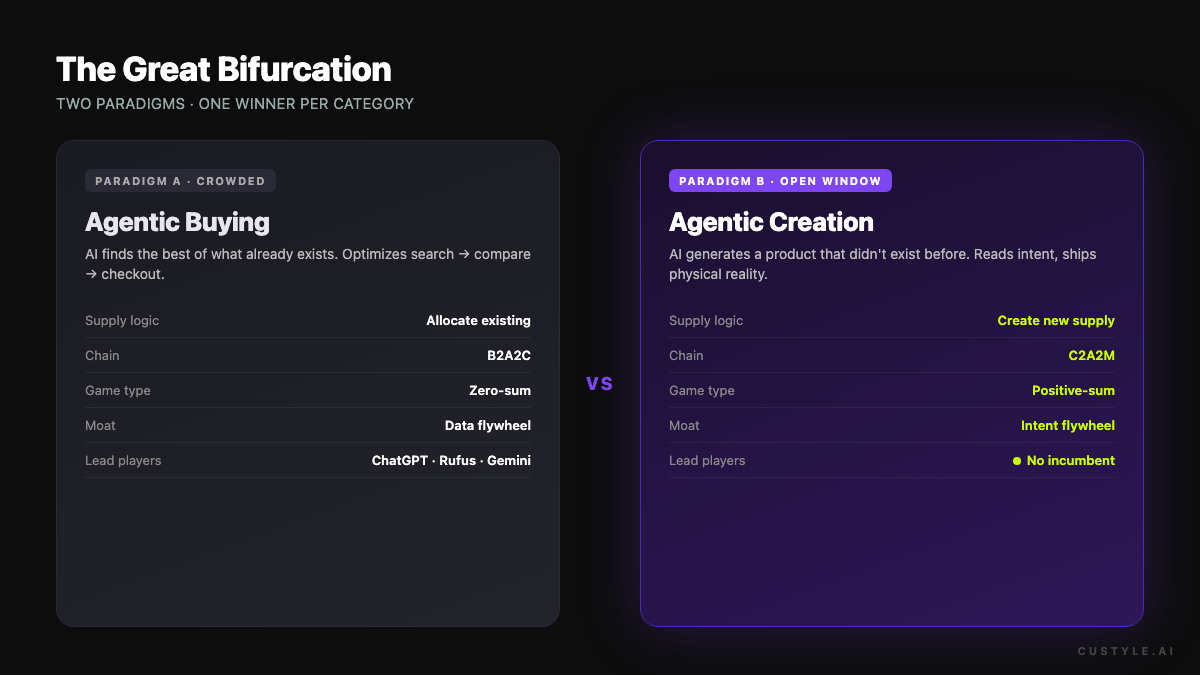

The Great Bifurcation: Agentic Buying vs. Agentic Creation

This is the report's central claim: commerce doesn't have one endgame. It has two.

| Dimension | Agentic Buying | Agentic Creation |

|---|---|---|

| Core action | Find the best of what exists | Generate something that doesn't |

| Agent role | Buyer — search, compare, negotiate, checkout | Creator — read intent, generate design, match process, schedule production |

| Supply logic | Allocate existing supply | Create new supply |

| Relationship chain | B2A2C (Brand → Agent → Consumer) | C2A2M (Consumer → Agent → Manufacturer) |

| Core moat | Data flywheel — more users, sharper recs | Intent flywheel — more conversions, sharper compilation |

| User psychology | "Find me the best" — cognitive offload | "Make my idea real" — creative participation |

| Endowment effect | Weak — no special bond with standard goods | Strong — co-creation builds psychological ownership |

| Value capture | Commission / ads (potential conflict of interest) | Creation service fee (incentive-aligned) |

| Market sizing | $3–5T (McKinsey, 2030) | Structurally underestimated. POD alone is $4.5B @ 11% CAGR |

| Lead players | ChatGPT Shopping, Amazon Rufus, Google Gemini | No category leader yet — wide-open window |

The headline: every billion-dollar AI commerce investment in the world is currently flowing into the left column. The right column has no incumbent.

This isn't because the opportunity is small. It's because Agentic Creation sits at a four-way intersection — AI intent compilation, flexible manufacturing, consumer psychology, protocol design — that very few teams stand on.

Why Top Analysts Missed It

Three reasons:

1. Cross-domain blind spot. Agentic Creation crosses AI, manufacturing, behavioral economics, and protocol design. Single-discipline analysts can't see the full chain.

2. Methodology anchoring. Standard market sizing is "current GMV × AI penetration." That formula can only measure Agentic Buying. It cannot measure supply that doesn't yet exist.

3. Incremental bias. The print-on-demand industry has existed for ten years, stuck at the "printing tool" mental model. Treating "AI design" as "image generation" is a category mistake. The leap from "print tool" to "intent → product agent" is a paradigm jump, not a feature upgrade.

5. C2A2M: Commerce Without the Brand Layer

The relationship chain is the part most people miss. Three eras, three topologies:

- B2C — Brand → Consumer. Zero-sum: Nike sells more, Adidas sells less.

- B2A2C — Brand → Agent → Consumer. Still zero-sum: brands compete to be ranked first by the agent.

- C2A2M — Consumer → Agent → Manufacturer. The brand layer is cut.

C2A2M is the only one of the three that is positive-sum. Every custom product is net-new supply — it doesn't take share from an existing brand's shelf. It expands the category boundary itself.

A user who normally buys three standard T-shirts may also pay $35 for a custom tee that finally captures their vibe. That $35 is a new wallet expansion, not a share shift.

Custyle is built on this topology. The moat is the intent flywheel — the more users describe what they want, the sharper the intent compiler gets, the higher the endowment effect, the higher the repeat rate, the more users describe what they want. Unlike the SKU flywheel of traditional retail, the intent flywheel accrues proprietary cognitive knowledge — what fuzzy expressions map to what design directions, for what audience, on what material, with what process.

This is not a database. This is a vocabulary of taste — and it doesn't transfer.

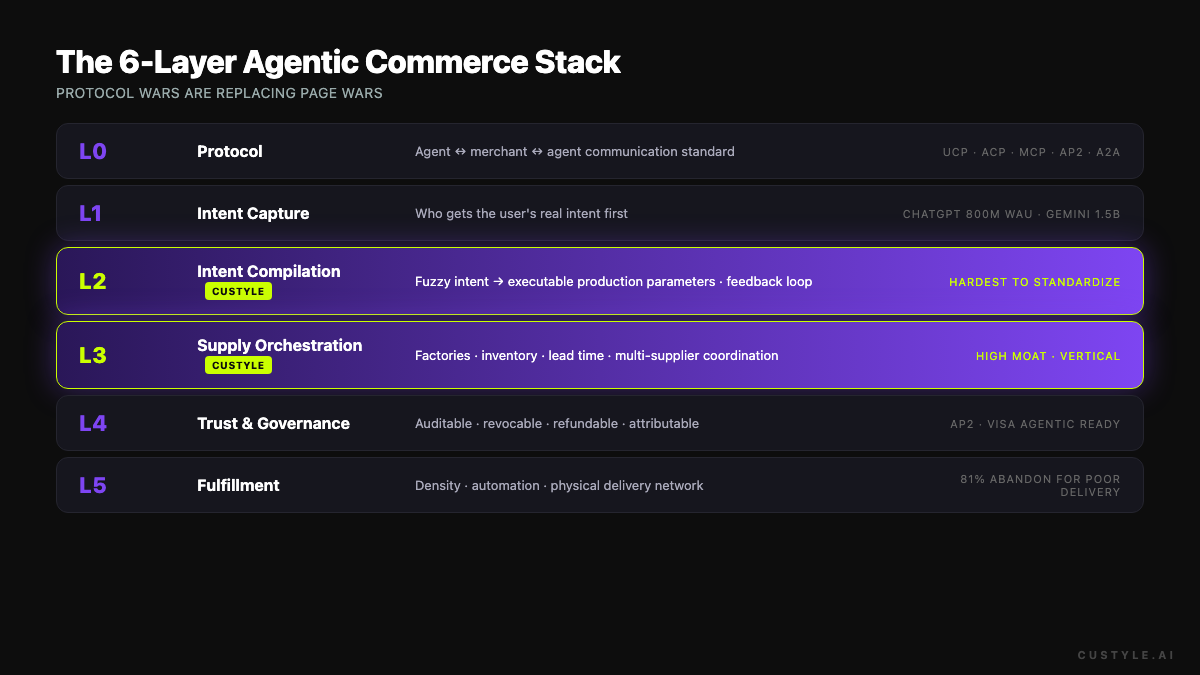

6. Protocol Wars Replace Page Wars

Value-chain rebuilds always start at the protocol layer. We're in one right now.

The new six-layer stack:

| Layer | Function | Moat | Current battle |

|---|---|---|---|

| L0 Protocol | Agent-to-merchant and Agent-to-Agent communication | UCP, ACP, MCP, AP2, A2A — whoever defines the pipe owns it | The HTTP fight of our era |

| L1 Intent capture | Who gets the user's real intent first | Distribution, content gravity | ChatGPT 800M WAU, Gemini 1.5B MAU |

| L2 Intent compilation | Translate fuzzy intent into executable parameters | Domain knowledge graph, production constraints, feedback loop | Hardest to standardize, highest moat |

| L3 Supply orchestration | Factory, inventory, lead-time, cost orchestration | Supply-chain data depth, multi-supplier coordination | Tradeoff optimization |

| L4 Trust & governance | Auditable, revocable, refundable, attributable | KYA, agent passports, signed authorizations | AP2, Visa Agentic Ready |

| L5 Fulfillment | Physical delivery network | Density, automation, scale | 81% of consumers abandon cart over delivery options (DHL) |

Strategic Warning to Every Brand and Builder

Whether your catalog is ACP/MCP compatible will decide whether AI agents can discover your products. This is the 2026–2028 equivalent of "is your site mobile-friendly?" in 2010. It is not a technical detail. It is a channel survival decision.

Why L2 Is the Real Startup Battleground

L1 is already taken. ChatGPT has 800M weekly actives. Gemini reaches 1.5B users monthly. Apple Intelligence and Android Gemini are baked into the operating systems. A startup competing for L1 with these giants will lose.

But L2 is wide open. L2 requires:

- A domain-specific knowledge graph — which designs work on which materials.

- Real-time production-constraint mapping — which supplier can deliver, in what window, at what cost.

- A closed feedback loop — user satisfaction with the physical result trains the compiler.

None of these three come for free with a general-purpose LLM. They have to be built inside a vertical, with real production data, over many cycles.

The right startup posture isn't "compete with ChatGPT for users." It is "become the default L2 backend ChatGPT calls when the task is Agentic Creation." L1 will consolidate to a few. L2 has room for dozens.

Custyle is building exactly here — the L2 + L3 stack for the AI Merch Agent category.

7. Category Order Decides Survival

Agentic Creation isn't one undifferentiated market. It's a category war won in a specific sequence. The first category to break must satisfy five conditions simultaneously:

- High design variability (users want to participate)

- Low production complexity (flexible supply can deliver)

- Standardized fulfillment (logistics cost is controllable)

- Low return risk (no fit/touch dependency)

- High emotional value (endowment effect fires hard)

| Priority | Category | Typical use | Why it goes first |

|---|---|---|---|

| First wave | T-shirts, hoodies, phone cases, mugs, tote bags | Fandom merch, gifts, team culture, self-expression | High design freedom, simple production, no sizing risk, strong emotional charge |

| Second wave | Posters, stickers, throw pillows, pet merch | Decor, walls, gifts | Simple production, but tighter preview accuracy required |

| Hold | Fitted apparel, furniture, fine jewelry | High ticket | Sizing risk, touch dependency, complex production, expensive returns |

AI + C2M's first bite is not "all of retail." It's the slice of retail that's expressive, simple to make, and predictable to preview. Build the closed intent-to-delivery loop there. Then expand.

This explains why the print-on-demand industry has been stuck at ~$4.5B with 11% CAGR for a decade. POD stayed at the "print tool" mental model. It never built the intent compiler, never closed the L2 loop, never went agent-native. The moment intent compilation + flexible supply + protocol compatibility combine in one stack, the category gets repriced.

That repricing is what Custyle is positioning for.

8. The Intent Flywheel: The New Defensible Asset

Traditional retail moats are built on the SKU flywheel — more SKUs attract more users, generate more data, sharpen recommendations. In Agentic Creation, the core asset is different. It is the mapping precision from intent to outcome.

The most valuable data is no longer "how many units of SKU X sold." It is:

- What kinds of fuzzy expressions map to what design styles?

- What audiences convert against what proposals?

- What previews lead to lower returns?

- What delivery promises lift repeat purchase?

Once this flywheel turns, the product starts to feel less like a website and more like a "vibe → merch" operating system.

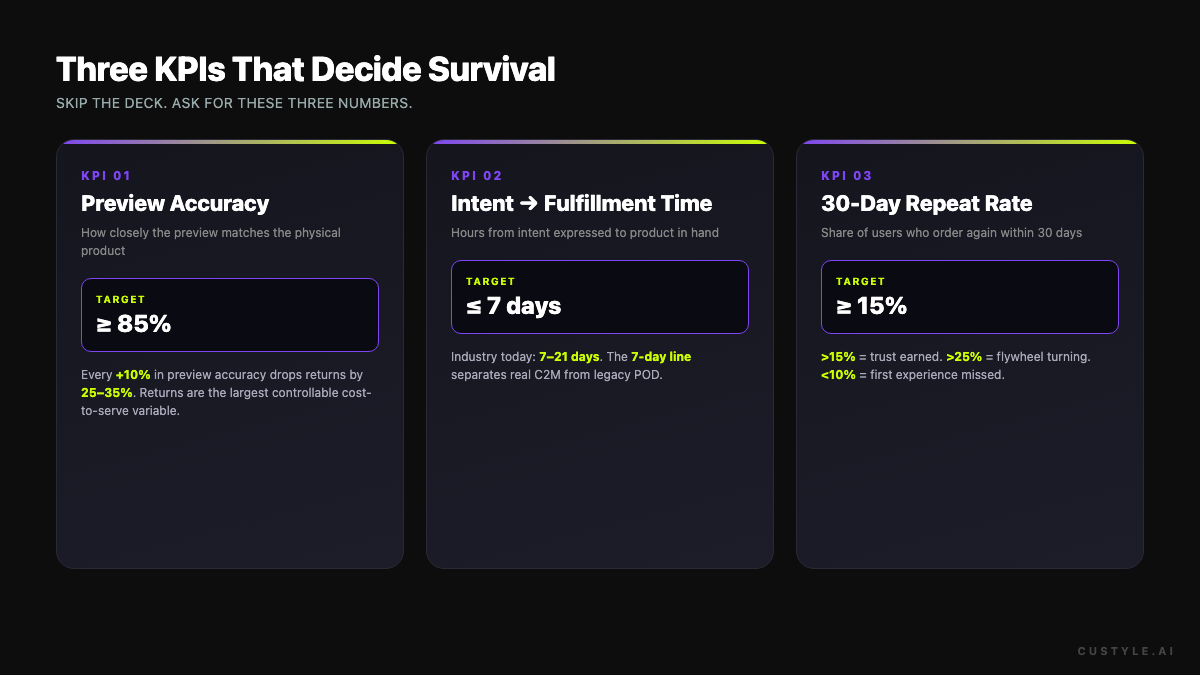

The Three KPIs That Decide Survival

| KPI | Definition | Why it kills you |

|---|---|---|

| Preview Accuracy | How well the preview matches the physical product | Direct line to return rate. Every 10% gain in preview accuracy can drop returns by 25–35%. Return rate is the largest controllable variable in cost-to-serve. |

| Intent-to-Fulfillment Time | Hours from intent expressed to product in hand | Industry today: 7–21 days. The 7-day threshold is where C2M and traditional POD separate. |

| 30-Day Repeat Purchase Rate | Share of users buying again within 30 days | >15% = trust earned. >25% = flywheel turning. Under 10% means the first experience didn't land. |

If you're evaluating an Agentic Creation startup, skip the pitch deck. Ask for these three numbers. If Preview Accuracy is below 85%, Intent-to-Fulfillment is above 7 days, and 30-day repeat is under 15%, the flywheel isn't turning — and without it, there's no moat.

9. The 2026–2028 Window

McKinsey's warning is worth quoting directly:

"By the time the customer-behavior shift shows up in your e-commerce KPIs, the laggards may already be too far behind to catch up."

Four curves cross between 2025 and 2028:

Curve 1 — Intelligence cost collapse. Inference cost dropped 280x in 18 months, from ~$20 to ~$0.07 per million tokens (Stanford AI Index 2025). What was uneconomical — generating a unique product for every user — is now production-grade.

Curve 2 — Flexible manufacturing maturity. China has 2.027M industrial robots in service (54% of the world). 2024 alone added 295,000 new units. 24-hour custom-order delivery is already running in pilot lines.

Curve 3 — Consumer demand maturity. The $2.3T emotion economy is real. 55% of consumers buy from recommendations. Gen Z consistently pays more for goods that fit their taste. Willingness to pay for "this is me" has crossed threshold.

Curve 4 — Protocol infrastructure forming fast. ACP, UCP, MCP, AP2, A2A all landed in the 2024–2026 window. The plumbing is being poured right now.

| Phase | Year | What's happening |

|---|---|---|

| Window | 2026–2028 | L3-grade products go mainstream. Protocols standardize. ~30% of transactions become AI-assisted. The only window to build category mind-share in Agentic Creation. |

| Restructure | 2028–2030 | UCP/ACP wire ecosystems together. B2A2C becomes dominant. Brands face "pipeline" risk. Agentic Creation unit economics turn positive. |

| Autonomy | 2030+ | L5 network-wide agents. "Predictive ambient commerce." Three-tier steady state: AI compute, trust hubs, global flexible supply. |

When ChatGPT's 800M weekly actives start handling custom merch tasks, the window closes. First-movers win on three accumulating assets: earlier intent understanding, deeper user trust, and a more mature AI → production parameter map.

10. What This Means If You're Building

If you're a founder: The hardest moat in 2026 is L2 intent compilation in a specific vertical. Don't fight L1 giants. Become the backend they need to call.

If you're a brand: Audit your catalog for ACP/MCP compatibility before Q4 2026. Treat it like the 2010 mobile-responsive transition — the cost of being late is invisibility, not lost revenue.

If you're an investor: Three KPIs cut through every pitch — Preview Accuracy ≥85%, Intent-to-Fulfillment ≤7 days, 30-day Repeat ≥15%. Anything below that is a POD tool, not an Agentic Creation platform.

If you're a creator or consumer: This is the first paradigm where your taste is the asset. The Endowment Effect, the IKEA Effect, and Flow theory all point at the same thing — what you make is worth more than what you find.

The endgame of commerce isn't "more products." It's less thinking, more certainty, more me. Agentic Buying delivers the first two. Only Agentic Creation delivers the third.

Custyle is building the AI Merch Agent for that third one — the L2 + L3 stack that turns intent into real, wearable, giftable, sellable merch. The window is open. Not for long.

FAQ

What is Agentic Creation?

Agentic Creation is the commerce paradigm where an AI agent generates a new, custom product from a user's intent — instead of searching for an existing product. It pairs intent compilation (L2) with flexible manufacturing (L3) to deliver one-off goods on the same economics that used to require mass production.

How is Agentic Creation different from Agentic Buying?

Agentic Buying optimizes the allocation of supply that already exists — search, compare, checkout. Agentic Creation generates supply that didn't exist before. Buying is zero-sum across brands. Creation is positive-sum across categories. The two run on different economics, trust dynamics, and moats.

What is C2A2M and why does it matter?

C2A2M stands for Consumer → Agent → Manufacturer. It's the relationship chain of Agentic Creation. The consumer expresses intent, an AI agent compiles it into production parameters, and a manufacturer fulfills it directly. The brand layer is skipped entirely, which is why C2A2M is positive-sum: every custom product is net-new supply, not share-shift.

Why does protocol compatibility matter for brands in 2026?

Protocols like ACP (OpenAI + Stripe), UCP (Google), MCP (Anthropic), and AP2 are becoming the standard way AI agents discover, evaluate, and transact with merchants. If your catalog isn't agent-readable, AI agents won't find your products. It's the 2026 equivalent of "is your site mobile-friendly?" in 2010 — and the penalty for being late is invisibility.

Why is the 2026–2028 window critical?

Four curves cross in this window: inference cost down 280x, flexible manufacturing maturity in China (2M+ robots), $2.3T emotion economy validating demand for taste-driven goods, and protocol standardization. After 2028, general-purpose agents like ChatGPT (800M weekly actives) absorb the category. First-movers gain compounding assets in intent understanding, user trust, and AI → production mapping.

Ready to make something?

Turn your ideas into real merch with AI. No design skills needed.

Start with a vibeArron Young

Founder, Custyle · May 19, 2026·19 min read

Further Reading

Explore all →Put a Legend's Name on Your World Cup Jersey

The official store said no. Messi, a retired legend, grandpa's name — here's the tribute World Cup jersey the store won't make you. Any name, any number.

Read more →

How to Make a Custom World Cup Jersey With AI (2026)

A custom World Cup jersey with AI means any name, any number, real typography — printed onto a real jersey and shipped, not a mockup. Here's how to make yours for 2026.

Read more →The Future of Brand Identity in AI Commerce: When Every Buyer Has an Agent

AI agents were supposed to demote brands to a backend API. The 2026 data says the opposite: AI sends high-intent buyers straight to brand.com. The new question is what you make.

Read more →

Creator Economy AI Tools 2026: AI Merch Agents Rise

The creator economy AI tools 2026 picture has one big shift: a new category — AI Merch Agents — taking the layer between creators and traditional print-on-demand.

Read more →